Last Updated on March 19, 2026

An M&A deal structure is the binding agreement that explains the terms and conditions when two companies decide to merge or when one company acquires another. It sets out the rights and obligations of the acquiring company and the target company, as well as the purchase price and how the deal will be carried out.

In mergers and acquisitions, the deal structure affects everything from ownership interests to which business operations and acquired assets are transferred. Whether it’s an asset acquisition, stock purchase, or a type of merger that forms a new legal entity, the structure you choose impacts tax benefits, risk, and the long-term business strategy for the companies involved.

What Is an M&A Deal Structure?

An M&A deal structure is the framework that defines how mergers and acquisitions are carried out. It’s a binding agreement that outlines the purchase price, the payment method, and how ownership interests in the target company will transfer to the acquiring company.

The structure also explains what happens to the target’s assets, liabilities, and business operations. For example, in some transactions the acquiring company might complete an asset purchase to select specific acquired assets like intellectual property, product lines, or equipment. In others, a stock purchase or share acquisition is used to gain a controlling interest in the target company.

Creating a proper deal structure can be complex. It requires balancing the goals of the companies involved, market conditions, financing options, and potential tax benefits. This is why investment banks, legal teams, and advisors play a major role in shaping the final terms.

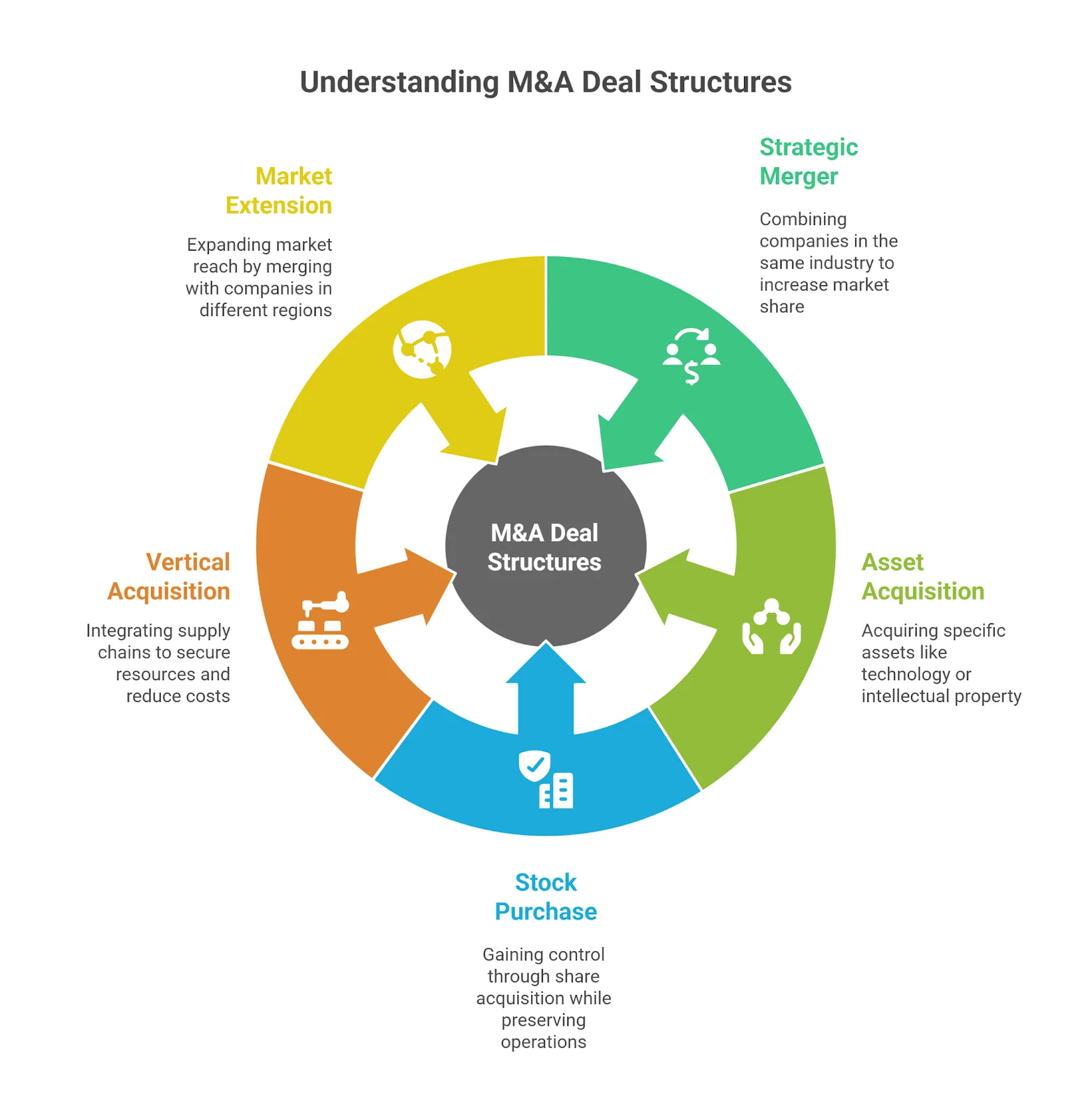

The Three Main Types of M&A Deal Structures

An M&A deal structure explains how two companies (or two or more companies) will combine and who gets what. The terms and conditions cover the purchase price, what the acquiring company buys, what the target company gives up, and how the legal entity changes.

A) Asset Acquisition

- How it works: The buyer purchases selected target’s assets (equipment, customers, intellectual property, product lines). The buyer can pick which acquired assets to take.

- Control & liabilities: Control of the business operations tied to the target’s assets shifts to the buyer. The buyer usually assumes only agreed liabilities. (Control still effectively moves to the acquirer.)

- When used: Buying a smaller target company, carving out a division, avoiding unknown debts, or when a private company acquires specific tech or brands.

- Deal notes: Often structured as an asset purchase; actual purchase price may be set using discounted cash flow and other methods; may deliver tax benefits.

B) Stock Purchase (Share or Interest Acquisition)

- How it works: The buyer acquires a controlling interest by share acquisition (or interest acquisition in an LLC), usually a majority of voting stock.

- Control & liabilities: The buyer now owns the target company (the same legal entity continues), so assets and liabilities stay inside the company the buyer controls.

- When used: Buying a private company or public company when keeping contracts, licenses, and employees in the same entity matters.

- Deal notes: Common in horizontal acquisitions (direct competitors or same customers), vertical acquisition (up or down the supply chain), or conglomerate acquisition (new industries).

C) Merger

- How it works: Two companies sign an agreement to combine. Either one becomes the surviving entity or they form a new legal entity. Both companies’ shares are typically surrendered in a classic merger.

- Control & liabilities: The combined business entity holds the assets and liabilities going forward.

- When used: To join forces in the same industry, grow market share, extend products or markets, or simplify ownership.

- Deal notes: A merger is one of the three traditional ways to structure mergers and acquisitions, alongside asset and stock deals.

Common Merger & Acquisition Variations (with quick cues)

| Type | What it means | Why choose it |

| Horizontal merger | Companies operating in the same market / direct competitors | Scale, market share, cost synergies |

| Vertical merger | Companies combine across the supply chain | Control inputs or distribution, margin gains |

| Conglomerate merger | Companies involved in unrelated industries | Diversification, new growth lanes |

| Market extension merger | Same products, new geography (market extension) | Enter new regions, access same customers type |

| Product extension merger | New product lines to the same customers | Cross‑sell, bundle, broaden offering |

| Statutory merger | One entity survives; the other disappears | Simpler post‑close structure |

| Statutory exchange | Buyer acquires control via share interest exchange | Flexible share-based consideration |

| Triangular merger | A wholly owned subsidiary is used to merge with the target | Liability and contract flexibility |

| Forward triangular merger | Subsidiary merges into the target | Target disappears; assets move to sub |

| Reverse triangular merger | Target merges into the buyer’s subsidiary | Target survives (useful for contracts/licenses) |

| SPAC (special purpose acquisition company) | Shell company takes a target public via merger | Faster path to public markets |

| Management acquisitions | Management team leads the acquisition deal | Continuity, aligned incentives |

Key Documents in Deal Structuring

Every M&A deal structure relies on clear documentation to guide the process. Two of the most important documents are the Letter of Intent (LOI) and the Term Sheet.

- Letter of Intent (LOI): A non-binding document that outlines the basic terms agreed upon by the acquiring company and the target company before detailed negotiations begin. It usually covers the purchase price, payment method, type of deal structure (such as asset acquisition or stock purchase), and any key conditions that must be met.

- Term Sheet: A summary of the major terms and conditions of the acquisition deal. It helps both sides confirm they agree on the framework before drafting final contracts.

These documents help prevent misunderstandings, guide legal teams, and set expectations for the companies involved. Having them in place early in the mergers and acquisitions process makes it easier to move from initial talks to closing the deal.

Examples of M&A Deal Structures in Practice

Seeing how M&A deal structures work in real situations can make the differences between them clearer.

Strategic Merger

A horizontal merger where two companies in the same industry and with the same customers combine to increase market share. A well-known example is when a public company merges with a direct competitor to become the surviving entity.

Asset Acquisition for Technology

An acquiring company completes an asset purchase to gain specific intellectual property and product lines from a smaller target company without taking on unwanted liabilities.

Stock Purchase for Brand Control

A private company acquires a controlling interest in another private company through a share acquisition, keeping the target company as a wholly owned subsidiary and preserving existing business operations.

Vertical Acquisition for Supply Chain

One company buys another in its supply chain to secure raw materials and reduce costs. This can be a forward triangular merger or reverse triangular merger, depending on whether the buyer uses a wholly owned subsidiary as part of the transaction.

Market Extension Merger

Two or more companies in the same market but in different regions combine to expand reach and customer base.

Factors That Influence the Right Deal Structure

Choosing the right M&A deal structure depends on more than just the purchase price. The acquiring company and target company must consider several factors that affect how the companies involved will operate after the transaction.

Key factors include:

- Business strategy: Whether the goal is to gain market share, expand into a new market, or secure supply chain advantages.

- Type of company: Different approaches may apply when a public company acquires a private company, or when a smaller target company merges with a larger one.

- Tax benefits: Certain structures, like an asset acquisition or forward triangular merger, can offer better tax outcomes.

- Financing options: How the acquisition deal will be funded can influence whether a stock purchase, interest acquisition, or asset purchase is best.

- Regulatory requirements: Some industries or same industry combinations require approvals that may favor a specific structure.

- Risk tolerance: The willingness to take on the target’s assets and liabilities may push the buyer toward an asset purchase instead of a stock purchase.

Understanding these factors helps ensure the deal structure supports both the short-term closing process and the long-term goals of the new business entity.

Key Considerations for Choosing a Deal Structure

When deciding on an M&A deal structure, both the acquiring and target companies must weigh how the choice will impact ownership, operations, and long-term goals. The structure should align with the overall business strategy, for example, a horizontal merger may be ideal for boosting market share, while a vertical merger can help strengthen the supply chain and enhance operational control.

Important factors to evaluate include:

- Strategic alignment – ensuring the structure supports the company’s market, operational, and growth objectives

- Risk exposure – in a stock purchase, the buyer assumes all assets and liabilities; in an asset acquisition, the buyer can select which assets and liabilities to take on, potentially limiting risk

- Purchase price and payment terms – deciding between cash, stock, or interest exchange, and understanding how structure impacts valuation

- Integration complexity – considering how easily the entities can be combined or maintained post-transaction

- Tax implications – assessing structures like a forward triangular merger that may offer significant tax advantages

Balancing these factors helps ensure the chosen structure supports both immediate transaction objectives and long-term business success.

Frequently Asked Question

1. What are the deal structures for M&A?

The main M&A deal structures are asset acquisition, stock purchase, and merger. Each transfers ownership and liabilities differently and has unique tax, legal, and operational implications.

2. What are the steps of an M&A deal?

Typical steps include identifying targets, signing a Letter of Intent (LOI), conducting due diligence, negotiating the deal structure and purchase price, drafting agreements, securing approvals, and closing the transaction.

3. What is the structured M&A process?

A structured M&A process is an organized sequence of tasks, planning, target search, valuation, due diligence, deal structuring, legal documentation, and integration, to ensure an efficient, compliant transaction.

4. What is the anatomy of an M&A deal?

The anatomy covers the transaction’s key parts: parties involved (acquiring company and target company), chosen deal structure, payment terms, legal agreements, and the post-closing integration plan.

5. What is the M&A deal model?

An M&A deal model is a financial model used to evaluate the impact of a transaction. It analyzes purchase price, funding sources, synergies, tax effects, and how the deal affects the buyer’s earnings and value.

6. What are the 4 types of mergers?

The four main types are horizontal merger (same industry competitors combine), vertical merger (companies in the same supply chain merge), conglomerate merger (unrelated industries combine), and market extension merger (companies in different markets join to expand reach).

Conclusion

The right M&A deal structure is essential for aligning the goals of the acquiring company and the target company while protecting their interests. Whether the transaction involves an asset acquisition, stock purchase, or some form of merger, the structure determines how ownership interests, liabilities, and business operations are transferred. It also shapes the purchase price, tax outcomes, and how easily the companies involved can integrate after closing.

A well-planned structure takes into account strategic fit, risk, valuation flexibility, integration needs, and potential tax benefits. By carefully analyzing these factors and working with experienced advisors, the parties can design a structure that maximizes value, reduces risk, and supports the long-term business strategy of the new entity or surviving entity.

Ready to structure your next deal with confidence? SmartRoom’s secure, fast, and simple virtual data rooms are built to handle the most complex M&A transactions. Explore SmartRoom and see how we can help you close deals more efficiently.

Matthew Small is the Vice President of Strategic Sales and Alliances at SmartRoom, where he builds partnerships and leads strategic efforts to deliver cutting-edge virtual data room solutions for dealmakers. With a strong background in enterprise sales and channel development, Matthew is passionate about unlocking new growth opportunities and helping clients navigate complex transactions with greater speed, security, and confidence.