Last Updated on March 23, 2026

Middle market private equity sits in a space where companies are big enough to be stable but small enough to grow fast. When you look at the middle market, you’re looking at more than 300,000 mid-sized companies across the U.S. These businesses make up a large share of the real economy and employ more than 40 million people. Many middle market companies are privately owned, often family-run, and ready for the next stage of growth. That’s why many private equity firms see this segment as one of the strongest places to invest.

If you’re exploring private equity investment, building an investment strategy, or helping guide a growing company, the middle market gives you a wide range of opportunities. You’ll find lower purchase multiples, less competition than large-cap deals, and more room to create value through operational improvements, growth equity, and strategic add-on acquisitions. It’s also where most private equity activity actually happens, middle market deals often make up 50–60% of all U.S. transactions.

This guide helps you understand how middle market private equity works, what makes these companies attractive, and what risks you need to watch closely. You’ll get clear definitions, practical tools, and simple checklists you can use to make better investment decisions, whether you’re an investor, advisor, operator, or part of a management team inside a mid-sized company.

What is Middle Market? Clear Definitions & Segmentation

When people talk about middle market private equity, they often mean companies that sit between small businesses and large public companies. But the term “middle market” isn’t exact, and many private equity firms use different definitions. That’s why it helps to know the common ranges used across the industry.

Common Ways the Middle Market Is Defined

Most middle market companies fall into these ranges:

| Metric | Typical Range |

| Annual Revenues | $10 million – $1 billion |

| Enterprise Value (EV) | $50 million – $500 million (typical PE target range) |

| EBITDA | Often $5 million – $50 million |

| Deal Size | Usually $25 million – $500 million |

| Fund Size Targeting This Segment | Roughly $200 million – $5 billion |

These ranges are not strict rules. They change based on sector, geography, leverage, and a firm’s investment strategy. But they’re widely used by middle market PE firms, investment bankers, and institutional investors.

Why Definitions Vary

The middle market can look different depending on:

- Sector: Tech or healthcare companies often trade at higher multiples than industrial or manufacturing firms.

- Geography: A “mid-market company” in the U.S. may count as a large business in another country.

- Growth stage: Mature companies with stable cash flow may qualify even with lower revenue.

- Deal structure: Leveraged buyouts, growth equity, private credit, and recapitalizations change how enterprise value is measured.

Because of these differences, always check how a data provider, fund manager, or advisor defines the middle market before comparing deals or performance numbers. Benchmarking mistakes are common when definitions don’t line up.

Simple Segmentation: Lower, Core, and Upper Middle Market

To make things clear, this guide uses three practical segments that reflect how many private equity firms evaluate targets.

1. Lower Middle Market (LMM)

The lower middle market is the starting point for many private equity firms.

Typical profile:

- Annual revenues: $5 million – $150 million

- Enterprise value: $25 million – $150 million

- Traits: Many private companies, often family-owned businesses or founder-led firms

- Why PE likes this segment: Lower purchase multiples, less competition, and room for value creation through operational improvements and financial engineering

- Common strategies: Growth capital, buy-and-build, strategic add-on acquisitions

This segment typically includes companies with solid products and early stability, but they may need help with systems, sales processes, or management depth.

2. Core Middle Market

This is the center of middle market PE activity and where most private equity investments happen.

Typical profile:

- Revenues: $50 million – $500 million

- Enterprise value: $150 million – $500 million

- Traits: Mature companies with stable cash flow and real growth levers

- Why PE likes this segment: Good balance of price, efficiency, and upside potential

- Common strategies: Buyouts, roll-ups, bolt-ons, recapitalizations, operational upgrades

Many private equity firms specialize here because core middle market companies are big enough to be stable but still agile enough to grow. They allow stronger value creation through operational improvements, strategic add-on acquisitions, and entry into new markets.

3. Upper Middle Market

The upper middle market acts as a bridge between mid-sized companies and larger public companies.

Typical profile:

- Revenues: $300 million – $1 billion

- Enterprise value: $500 million – $1.5 billion

- Traits: Highly established companies with larger management teams and predictable earnings

- Why PE likes this segment: Larger deal sizes, strong processes, easier bolt-on execution

- Competition: Higher, more strategic buyers and larger PE firms enter this range

This segment starts to resemble large cap targets, but still offers a wider field of opportunities than mega-deals.

Why Segmentation Matters

You should get clear on how a fund or advisor defines the middle market before making any investment decisions. Definitions affect:

- How you compare entry valuations

- What performance benchmarks you use

- How you judge leverage, risk, and returns

- Which exit strategies make sense

- The investment process and due-diligence depth

Since middle market consists of many private companies with different financial structures, aligning definitions helps you avoid bad comparisons and misleading deal analysis.

The Middle-Market PE Ecosystem: Typical Deals, Targets & Why It Appeals

The middle market private equity ecosystem is built around buying and growing mid-sized companies that are stable but still flexible enough to scale. Because the middle market consists of more than 300,000 private companies, you see far more investment opportunities here than in large cap deals. In fact, middle market deals make up about 50–60% of all U.S. private equity transactions, and around 75% of global deal volume.

Below is a clear look at the deal types, target companies, and the core reasons this segment appeals to many private equity firms and investors.

Typical Middle-Market Deal Types

Most middle market deals fall into a few common categories. These deal types let private equity investors shape the company’s future through growth, new markets, and operational improvements.

- Private-to-Private Buyouts: These involve buying established mid-sized companies from founders, family owners, or other private sellers. Many middle market companies fit this profile because they have stable cash flow but need help scaling.

- Management Buyouts (MBOs): Here, the management team partners with a private equity firm to buy the company. PE firms provide the private equity capital, and the team drives growth during the investment period.

- Growth Equity Deals: Growth equity gives companies capital for hiring, technology, or entering new markets without giving up full control. This is common for mid market companies that want to expand quickly.

- Roll-Ups, Bolt-Ons & Add-On Acquisitions: One clear fact about middle market private equity:

PE firms often pursue bolt-on acquisitions to consolidate fragmented industries and grow market share.This “buy and build” strategy helps a platform company become a much larger player by adding complementary businesses. - Carve-Outs and Recapitalizations: These deals involve buying divisions from larger companies or restructuring the capital stack. They let you capture value from mature companies that need new leadership or a clearer strategy.

Profile of Typical Target Companies

Middle market PE firms usually look for companies that are:

- More established than small-cap firms, but more agile than large-cap targets

- Generating $10 million to $1 billion in annual revenues

- Valued between $50 million and $500 million in enterprise value

- Showing strong cash flow, consistent revenue growth, and a solid management team

- Able to benefit from clear growth levers such as operational improvements, new markets, or add-on acquisitions

A proven track record of profitability is a major factor in private equity investment decisions.

Why the Middle Market Remains Structurally Appealing

Several built-in advantages make this segment attractive to private equity investors, institutional investors, and strategic buyers:

A Large Universe of Opportunities: Middle market represents the biggest share of private companies in the U.S., giving you more investment opportunities than the large-cap space.

Less Competition and Better Pricing: Most middle market firms face fewer bidders, which often leads to lower purchase multiples and more room for upside.

Strong Return Potential: Middle market private equity investments often outperform large cap deals because returns come from:

- Operational improvements

- Growth initiatives

- Strategic add-on acquisitions

- Multiple expansion

These drivers matter more here than pure financial engineering.

More Flexible Capital Structures: Middle market deals typically use less leverage than mega-deals. This lowers financial risk during economic uncertainty or rising interest rates.

Appeal Across Sectors: Tech, healthcare, and business services led the space in early 2024, making up about 60% of transaction value, showing where most PE firms focus their deal sourcing efforts.

What the Data & Research Show: Performance, Growth & Value Creation under PE Ownership

When you look at the research, middle market private equity stands out for its ability to create value through operational improvements, stronger management teams, and strategic add-on acquisitions. While results vary by sector and timing, the data shows that many middle market companies improve their performance under private equity ownership.

Stronger Performance and Productivity Gains

Studies across the private markets show that companies purchased by private equity firms, especially mid-sized companies, often see:

- Better productivity

- Higher revenue growth

- Clear improvements in margins and cash flow

A major reason is the hands-on support that middle market private equity firms provide. These firms usually focus on active management, building better systems, tightening financial analysis, and supporting management teams with industry specialists.

Because middle market consists of companies that are big enough to scale but small enough to change quickly, you see stronger results here than in many large cap deals.

Profitability and Margin Expansion

Middle market private equity firms rely less on financial engineering and more on direct value creation. Research shows that:

- Companies often improve EBITDA margins during the investment period

- Strategic add-on acquisitions accelerate growth in both revenue and market share

- Operational improvements drive most of the value, not just leverage

This is one reason middle market investments often yield higher returns compared to large cap deals. You capture both performance gains and multiple expansion when the company sells.

Why Outcomes Vary Across Deals

Even though the middle market represents a strong area for private equity investment, results are not uniform. Several factors influence returns:

- Macroeconomic cycles: Economic uncertainty, interest-rate spikes, and weak credit markets can stress mid market companies.

- Sponsor quality: The experience of the private equity firm heavily affects performance. Funds with sector specialization often outperform generalists.

- Timing: The investment period and exit environment matter. Rising interest rates have slowed private equity activity and extended holding periods across many funds.

- Sector: Tech, healthcare, and business services currently lead middle market private equity activity, but each sector responds differently to market pressure.

These differences explain why some portfolio companies outperform while others face significant challenges.

What’s Still Hard to Measure

Even though middle market private equity represents a large share of deal activity, it is still under-researched because:

- Many private companies do not report financials publicly

- Definitions of “middle market” differ across data providers

- There isn’t consistent, long-term data segmented by enterprise value, revenue, or deal size

- Many exits are private sales to strategic buyers or financial buyers, not IPOs, so public data is limited

Despite this, the overall evidence is clear: middle market private equity can be a strong engine for value creation, especially when you combine operational improvements, sector expertise, and strong management teams.

Risks, Challenges & What Can Go Wrong with Middle-Market PE Deals

Middle market private equity offers strong opportunities, but it also carries real risks. Many middle market companies operate with tighter budgets, smaller teams, and less room for error than larger companies. If you’re evaluating middle market deals, you need a clear view of the issues that can slow down value creation or put your investment at risk.

Debt and Financing Risk

Most middle market deals use a mix of equity and debt. While middle market PE firms usually use less leverage than mega-deals, debt is still a major part of the capital structure. Rising rates and tighter credit markets can create significant pressure.

Key risks include:

- Interest-rate spikes that increase debt servicing costs

- Refinancing risk if lenders pull back during economic uncertainty

- Liquidity challenges when cash flow drops or growth slows

Many private equity firms have felt this pressure recently, as higher interest rates have slowed both private equity deployment and exit activity.

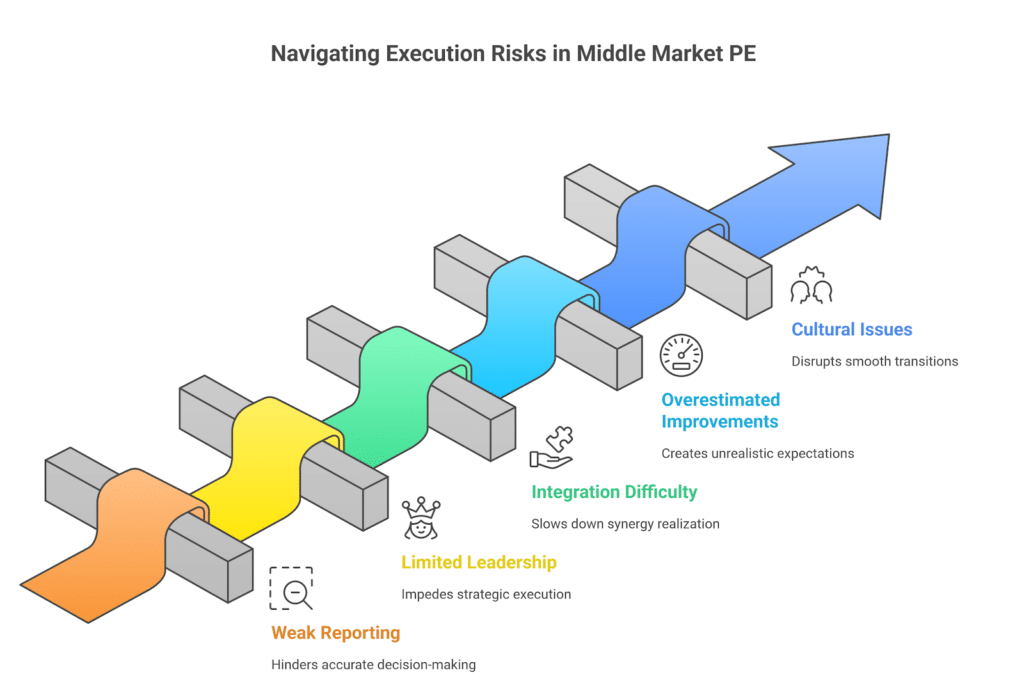

Execution Risk

Value creation in middle market PE depends heavily on your ability to make operational improvements, support management teams, and follow a clear investment strategy. The problem is that many middle market businesses lack the deep infrastructure larger companies have.

Common execution challenges include:

- Weak or incomplete financial reporting

- Limited leadership depth

- Difficulty integrating add-on acquisitions

- Overestimating the speed of operational improvements

- Cultural issues in family-owned businesses transitioning to new ownership

If improvements take longer than expected, returns can drop quickly.

Benchmarking & Comparability Risks

A major issue in middle market private equity is that definitions vary across private equity firms, fund managers, and data providers. One firm may classify a $150 million enterprise value deal as lower middle market, while another calls it upper middle market.

This creates risks when you try to compare deals, including:

- Misleading performance comparisons

- Survivorship bias from only looking at successful portfolio companies

- Selection bias from studying only publicly reported deals

If you don’t align definitions, your benchmarks, multiples, and forecasts can be way off.

Market & Macro Risks

Middle market businesses have fewer buffers than large corporations. They can be hit harder by:

- Economic downturns

- Sector-specific declines

- Supply chain disruptions

- Volatile exit markets

Research shows this clearly: when the economy slowed in 2022, middle market deals dropped only 19%, but large cap deals fell nearly 40%. Even though middle market activity is more resilient, the individual companies inside these deals still face real pressure.

Exit strategies also become harder during weak markets, especially since over 90% of small and middle market exits go to strategic buyers or other financial buyers, not IPOs. If buyer demand slows, exits can take much longer.

What All This Means for You

Middle market private equity can deliver strong returns, but only when you understand the risks and plan for them early. You need to:

- Stress-test interest rate and cash flow assumptions

- Evaluate management teams with care

- Be realistic about operational improvement timelines

- Check definitions before benchmarking deals

- Watch credit markets and exit conditions closely

When you handle these challenges with discipline, middle market PE offers real potential. When you ignore them, deals can break quickly.

Middle-Market PE from the Stakeholder’s Lens: What It Means for Investors, Deal Teams, Legal & Founders

Middle market private equity affects every group involved in a deal differently. Whether you’re an investor, advisor, lawyer, founder, or part of a management team, you play a major role in shaping the investment strategy and creating value. Understanding how middle market deals impact your responsibilities helps you make better decisions and avoid costly mistakes.

For Investors & Limited Partners

As an investor or LP, the middle market gives you a strong mix of opportunity and risk. Middle market investments often outperform large cap deals because returns come from operational improvements, revenue growth, and strategic add-on acquisitions, not only financial engineering.

Here’s what matters most to you:

- Risk/Return Profile: Middle market private equity offers upside potential with more reasonable entry valuations. You also get diversification because many middle market firms operate in different industries and regions.

- Sponsor and Fund Diligence: Fund managers matter. Sector specialization, track record, deal sourcing quality, and capital discipline affect your long-term returns.

- Vintage Timing: Private markets shift fast. Rising interest rates and slower exits have affected fundraising and distributions, so evaluating timing is key.

- Capital Structure: Middle market firms typically use less leverage than larger PE firms, which lowers financial risk but requires stronger operating results.

If you invest with discipline and realistic expectations, middle market private equity can be a strong addition to your portfolio.

For Corporate Finance & M&A Teams

If you’re part of a corporate finance or M&A team, you handle much of the heavy lifting in a middle market deal.

Before the deal, you can expect:

- Deep financial analysis and detailed data-room work

- A full review of revenue quality, cash flow strength, and operational systems

- Closer collaboration with bankers, strategic buyers, and private credit lenders

After the deal, your focus shifts to:

- Integrating bolt-ons or complementary businesses

- Supporting operational improvements

- Tracking performance during the investment period

- Preparing the company for exit strategies, often a sale to another PE firm or a strategic buyer

Because most middle market firms lack complex internal systems, your work shapes the foundation of future value creation.

For Legal, Compliance & Risk Teams

Middle market PE deals require careful legal and risk planning. You help make sure the company’s structure, governance, and financing terms support long-term success.

Key responsibilities include:

- Reviewing debt terms, covenants, and refinancing risk

- Building governance structures that fit the company’s size and management style

- Stress-testing scenarios like interest-rate swings, liquidity challenges, or slower revenue growth

- Preparing for exit options, which are usually private sales, not publicly traded IPOs

Since many mid market companies lack the compliance infrastructure of larger public companies, your guidance helps prevent major issues later.

For Founders, Operators & Company Owners

If you’re a founder or operator, a middle market private equity deal can be a turning point for your business. It brings growth capital, industry expertise, and new resources, but also changes in governance and expectations.

You should understand:

- Trade-Offs: PE firms bring operational expertise, strategic planning, and a stronger management team, but they also introduce new reporting requirements, leverage, and clearer performance targets.

- Deal Structure: Know how the initial investment is structured, what ownership you keep, and how carried interest or earn-outs work.

- Growth Expectations: PE ownership focuses on value creation through operational improvements, new markets, and add-on acquisitions.

- Exit Planning: Private equity investors think ahead. Most middle market exits happen through sales to strategic buyers or financial sponsors.

When you know what to expect, you can choose a partner that fits your vision and timeline.

How to Evaluate & Benchmark Middle Market PE Opportunities: A Practical Framework

When you’re looking at middle market private equity opportunities, you need a simple way to judge whether a deal is worth pursuing. Because middle market consists of companies with different sizes, structures, and growth paths, having a clear framework helps you compare deals, stress-test assumptions, and avoid major mistakes. Use the checklists and tools below to strengthen your investment decisions.

Pre-Deal Evaluation Checklist

Before you commit to a middle market investment, review the fundamentals of the company and deal structure. This helps you understand both the upside and the risks.

Key Questions to Ask

- Company Size: Does the business fit typical middle market ranges for annual revenues, EBITDA, and enterprise value?

- Sector Strength: Is the sector stable, growing, or exposed to economic uncertainty?

- Management Team: Is the leadership experienced enough for a private equity environment?

- Cash Flow Stability: Can the company handle debt servicing? What happens if revenue dips?

- Growth Levers: Are there realistic ways to improve value, such as operational improvements, new markets, or add-on acquisitions?

- Debt Capacity: How much leverage can the company support without creating financial stress?

- Exit Readiness: Is the business attractive to strategic buyers or financial buyers down the road?

These basics help you spot whether the company is set up for value creation or facing significant challenges.

Key Metrics & Benchmarks to Stress-Test

Below is a simple table you can use to benchmark common middle market deal metrics.

| Metric | Typical Middle Market Range / Insight |

| EBITDA Multiples | Often lower than large cap deals, giving you room for multiple expansion |

| Debt / EBITDA | Usually lower leverage than mega-deals (often 2.5x–4.5x) |

| Hold Period | 4–7 years for most middle market PE deals |

| Value Creation Mix | Driven by operational improvements, revenue growth, and add-on acquisitions |

| Exit Multiple Assumptions | Should remain conservative due to rate environment and slower exits |

Good deals usually offer both operational upside and realistic paths to exit, not just financial engineering.

Risk-Adjusted Scenario Planning

Strong middle market private equity deals are built on clear scenario planning. You should model how the company performs under different economic and market conditions.

Build Three Simple Cases

- Base Case: Realistic revenue growth and margin expansion

- Upside Case: Strong execution, successful add-on acquisitions, and healthier market conditions

- Downside Case: Interest-rate spikes, slower revenue growth, tightening credit markets, or rising costs

This helps you understand whether the company can withstand shocks, especially since mid market companies have less financial cushioning than larger public companies.

Due-Diligence & Red-Flag Checklist

Use this checklist to catch common issues in middle market deals before they become costly.

What to Verify

- Management Depth: Is the team strong enough? Or too dependent on one key leader?

- Governance: Are controls and reporting systems strong enough for private equity ownership?

- Operational Improvement Potential: Are the proposed changes realistic, or too optimistic?

- Leverage Risk: Does the company rely on debt or can it grow with less leverage?

- Cash Flow Quality: Are earnings stable or overly adjusted?

- Exit Sensitivity: Will strategic buyers or financial sponsors still be interested if market conditions weaken?

- Transparency: Are financials clear, or are there gaps and inconsistencies?

If too many red flags pop up, the deal may not support your investment strategy or return goals.

How This Framework Helps You

By using this structure, evaluating the company, benchmarking metrics, running scenarios, and checking for risks, you can make smarter middle market PE decisions. It keeps you focused on the fundamentals that matter most in middle market investments, where success depends on active management, strong cash flow, and realistic value-creation plans.

Frequently Asked Questions

1. What Does Middle Market Mean in Private Equity?

In private equity, the middle market refers to companies with $10 million to $1 billion in annual revenues and $50 million to $500 million in enterprise value. These mid-sized companies are large enough to be stable but small enough to benefit from operational improvements, growth initiatives, and add-on acquisitions. Middle market private equity represents the majority of PE activity and offers strong opportunities for value creation.

2. What is The Difference Between Mid-Market PE And Large-cap PE?

Mid-market private equity focuses on buying and improving mid-sized companies, typically with lower purchase multiples, less leverage, and more operational value creation. Large-cap PE targets bigger companies with higher valuations, more competition, and heavier reliance on financial engineering. Mid-market PE tends to offer more flexibility, more realistic pricing, and greater room for strategic growth.

3. What is Considered Lower Middle Market Private Equity?

Lower middle market private equity targets smaller mid-sized companies with $5 million to $150 million in annual revenues and $25 million to $150 million in enterprise value. These businesses are often founder-led or family-owned and provide strong opportunities for buy-and-build strategies, operational upgrades, and growth capital injections. This segment also tends to have less competition and more attractive entry valuations.

Conclusion

Middle market private equity remains a strong area of opportunity because mid-sized companies offer a mix of stability, flexibility, and room for improvement. With over 300,000 middle market businesses in the U.S. and most private equity deals occurring in this segment, you get reasonable entry valuations and multiple ways to create value through operational improvements, revenue growth, and strategic add-on acquisitions. These companies also tend to move faster than large corporations, giving you clearer paths to drive performance during the investment period.

But middle market investments also come with real risks. Debt servicing pressure, interest-rate swings, weaker internal systems, and limited management depth can all impact results. Because mid market companies have fewer financial buffers and inconsistent definitions across data providers, you need disciplined evaluation, clear metrics, and realistic scenario planning. When you combine strong fundamentals with careful oversight, middle market private equity can offer compelling long-term returns.

Executing well requires more than strategy, you need secure data sharing, organized workflows, and fast access to the right information throughout the deal process. If you want a smoother way to manage diligence or prepare a company for a sale, SmartRoom offers a secure, simple, and fast virtual data room built for complex deals like middle market M&A, fundraising, and audits.

Patrick Schnepf is the Senior Vice President of Global Sales at SmartRoom, where he leads strategic initiatives to enhance secure file-sharing and collaboration solutions for M&A transactions. With a career spanning over two decades in sales and business development within the technology sector, Patrick has been instrumental in driving SmartRoom’s global revenue growth and expanding its market presence. He is a growth-oriented leader who excels at building go-to-market strategies that accelerate adoption, deepen customer relationships, and business impact.